The AI infrastructure race is at full speed in Canada. $100+ billion in new data centre investment is flowing in over the last two years alone, drawn by our clean electricity grids and cold climate. Microsoft, AWS, Google, TELUS, and Bell are all deploying capital here right now, making Canada a new frontier for AI infrastructure.

But building this big, this fast, creates problems for our climate that haven't been solved yet.

Speed to power - how fast a new facility can actually get connected to the electricity grid - is the number one bottleneck holding back new data centre projects. And without advances in clean energy, efficient hardware, cooling, grid integration, and circular materials, the rush to get projects online will force tradeoffs on emissions, water, waste heat, and grid capacity that will be locked in for decades.

What it looks like to build “clean compute” - running this infrastructure on clean energy, with minimal water use, recovered waste heat, and a path to net-zero emissions - is being decided in every project. Not in five years. Right now.

Made-in-Canada solutions can accelerate the clean compute transformation, and companies across the country are already starting to pick up the challenge.

From speaking with founders, investors, and technology innovators across Canada, we've mapped the opportunity landscape for Canadian startups, from incremental improvements to paradigm-shifting disruption.

We identify who the buyers are and what they actually need, where we see the strongest disruption opportunities, and what the real risks are for founders and investors trying to commercialize and scale in this market.

STATE OF PLAY

Canada is on the cusp of an unprecedented buildout of data centres to support the AI industrial revolution.

For decades until the ChatGPT Big Bang of 2022, data centres grew modestly and predictably. AI changed the game for data centre growth, requiring massive amounts of computing capacity to train new models and run AI tools. AI chip racks can draw 10x more electricity than typical compute workloads, generate 10x more heat than traditional servers, and a single AI query uses 10x more energy than a traditional Google search.

Canada is expecting exponential growth, with more than 9GW of projects in the development pipeline compared to just 1.4GW of live capacity.

By the numbers:

Alberta: 11.9 GW of data centre connection requests in Q1 2025 alone - more capacity than the entire province added in the past decade

Ontario: Data centre load projected to grow from 2.5 TWh today to 14 TWh by 2050, representing 4% of total provincial demand by 2035

Quebec: Expects 4.1 TWh of new data centre demand between 2023-2032

Current state: 239 data centres operating as of 2024, concentrated in Ontario and Quebec

US comparison: 567 operating facilities with 13,635 MW capacity and 630 planned projects adding 145,063 MW

In context: Alberta's largest data centre connection request is 1,800 MW - the equivalent of adding another Calgary to the grid

The amount of electricity used by Canadian data centres has increased by 50% since 2021, and utilities are projecting data centre demand to grow 400% or more by 2050, with hundreds of new facilities consuming enough electricity to power 3 million Canadian homes.

And it's not just electricity. Data centres need land and water, and while the exact footprints are still emerging, a mid-size project in the US can consume around 110 million gallons/year.

WHO’S INVESTING

Despite some uncertainty about timing and scale, hyperscaler commitments signal real momentum:

Microsoft: $19B (2023-2027) for Canadian cloud expansion

AWS: $17.9B through 2037 across Canada West

Telus: $70B network infrastructure drive including data centres and emissions reductions

Bell: Building a national data centre network, including 6 data centres in BC

Billions are flowing into data centre infrastructure and Canada plans to build out 9+ GW of compute with one of the cleanest grids in the world. Yet new projects are turning to natural gas for reliability.

Startups that can help operators reduce energy consumption, decarbonize power supply, eliminate water use, or recover waste heat have a massive, urgent buyer base.

JOIN OUR CLEAN COMPUTE ROUNDTABLE

We're hosting a curated roundtable to present key findings from the report and dig into the opportunities with founders, investors, and operators building in this space.

Spots are limited. Sign up to be notified when registration opens.

HOW IT’S SHAPING UP

The number one chokepoint for data centre developers is speed to power.

Data centres need to get online as fast as possible, but grid connection requests take years to process. Canada has abundant clean power (>80% non-emitting) but connecting a 500 MW facility means years of queue time, regulatory approvals, and transmission buildout.

Operators facing deployment pressure hit a fork: wait for clean grid access, or build your on-site generation and get moving.

Hyperscalers have net-zero and clean energy targets, but also customers who want them online yesterday, creating tension between speed to market and sustainability:

Natural gas generators offer speed and flexibility but lock in emissions for 20-30 years and face supply chain backlogs

Renewables have zero emissions and are closing the speed gap, but have larger footprints and require storage for reliability

SMRs and enhanced geothermal promise clean baseload power, but face long lead times and permitting obstacles

Islanded microgrids let data centres get up and running quickly while transmission catches up, but require overbuilding for reliability

Power strategies are evolving quickly, but the choices made in the next 3-5 years will lock in emissions profiles for decades.

SIX CORE CHALLENGES

Speed to clean power dominates, but operators are navigating six interconnected constraints, each one a market opportunity for startups that can solve it:

Cooling: AI processors generate 10x more heat per rack than traditional servers. Air cooling struggles for high performance racks above 20kW. Liquid cooling works but consumes millions of litres a day and requires retrofits.

Efficiency: The cleanest megawatt is the one you don't need. Chip efficiency, workload optimization, and smarter infrastructure design are all levers that operators are pulling hard.

Clean power: Even grid-connected facilities need backup for five nines of uptime (99.99999%). Diesel generators are tried and tested. Natural gas turbines offer more capacity but face growing supply chain backlogs. Clean alternatives exist but can be more expensive to install.

Grid integration: Constrained grids need large load customers that can offer more than just demand. Flexible loads, grid services like peak shaving, and demand response can accelerate connection times and make a more resilient grid.

Embodied carbon: Construction materials account for 20-30% of a data centre’s lifecycle emissions. Speed-to-market pressure pushes builders to stick with high-carbon defaults.

Hardware churn: AI hardware evolves fast, with 3-5 year refresh cycles and accelerating. Old servers pile up. Critical minerals and rare earths are waiting to be recycled.

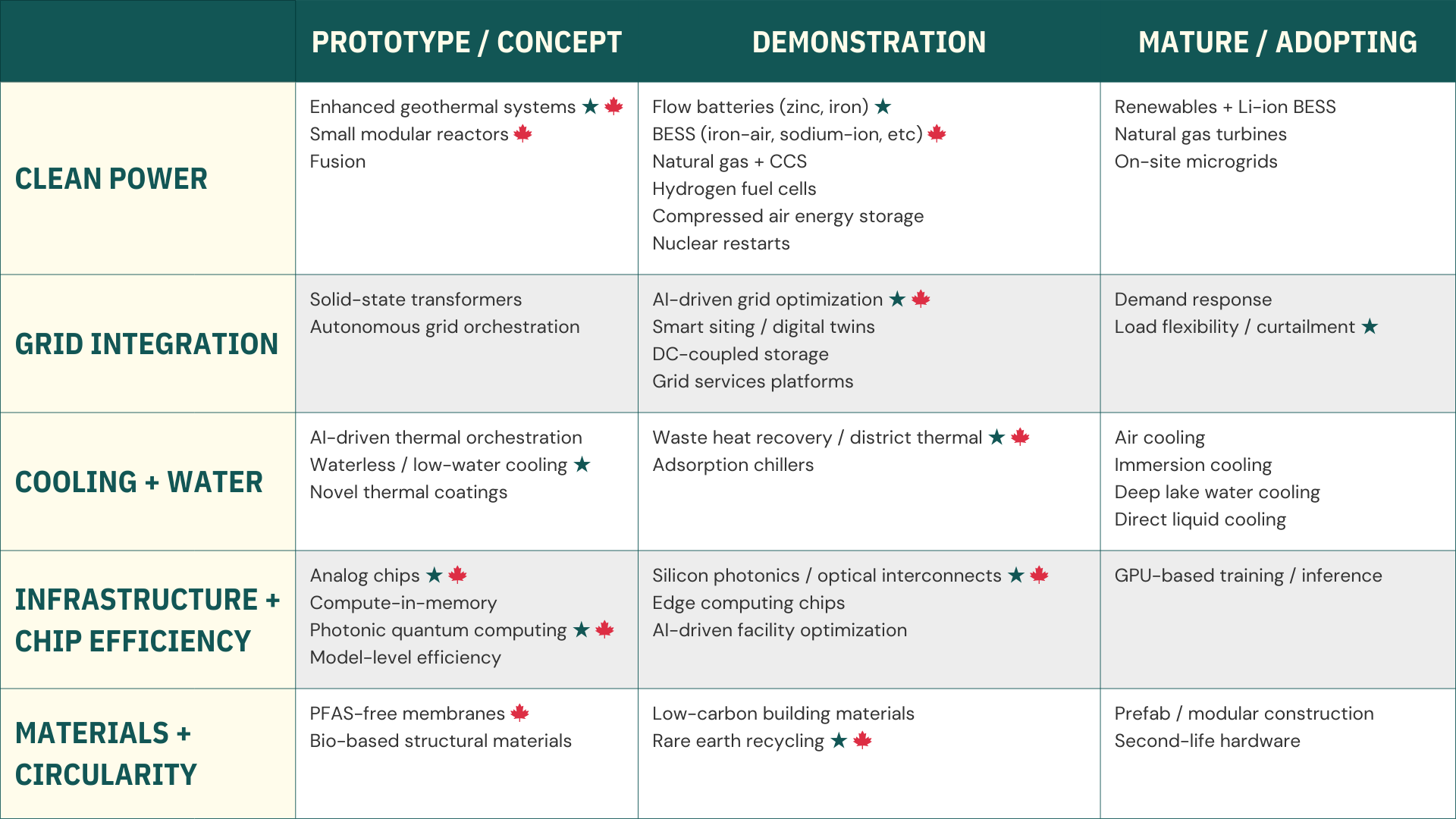

TECHNOLOGY LANDSCAPE

We mapped the different technology opportunity areas that are solving these six core challenges, from the earliest prototypes and pilots through to adoption and deployment in the field. Across this broad spectrum, we identified two key segments:

1) High-conviction disruption. These are technologies we see as true paradigm shifts - not incremental improvements. Fusion-like clean energy through enhanced geothermal; replacing copper wires with optical interconnects; grid flexibility to unlock GWs of energy.

2) Structural Canadian advantages or enabling strengths. Resource, talent and innovation bases that create the conditions to lead in specific technology areas. Canada doesn’t necessarily have a monopoly on these (many countries have clean grids or natural resources), but they are a strong platform to build on. More on this in a moment.

Across clean compute’s biggest challenges, the strongest opportunities for Canadian startups sit at the demonstration and prototype stage, where disruption potential meets Canadian strengths.

Maturity categories adapted from the IEA Clean Energy Innovation framework. See Appendix.

★ = highest-conviction disruption opportunity 🍁 = Canadian home advantage

DISRUPTION OPPORTUNITIES

If you’re a founder or investor in this space, these are the areas where disruption potential and Canadian home advantage converge: the strongest bets we see across the landscape.

Behind-the-meter clean power. Enhanced geothermal, energy storage, and SMRs converge on the single biggest bottleneck: delivering 24/7 clean power without waiting years for grid connection. Canada has structural enablers in all three (drilling expertise, critical minerals, nuclear regulatory leadership and expertise).

Category leaders: Eavor, Rodatherm, e-Zinc, Moment Energy, ARC Clean TechnologyEfficiency. Silicon photonics, analog chips, and model-level efficiency attack the root cause: reducing how much energy computation requires in the first place. Photonics and semiconductor clusters in Ottawa and Montreal plus the $223M FABrIC initiative give Canada unique end-to-end capability and depth. Hyperlume’s acquisition by Credo (2024) proves the exit thesis. Impact compounds as inference overtakes training as the dominant workload.

Category leaders: Hyperlume (acquired), BlumindCooling innovation. Waste heat recovery, adsorption chillers, and waterless cooling systems address the thermal challenge while turning an energy liability into a community asset. Canada’s cold climate offers a structural cooling advantage and makes district thermal economics viable.

Category leaders: XNRGY, Enersion, CorixHardware churn. PFAS-free membranes, rare earth recycling, and second-life hardware platforms address the full material lifecycle. Cyclic Materials is already commercializing. As hardware refresh cycles accelerate and PFAS bans expand, the regulatory pull only strengthens. Canada brings a depth of experience across the rare earths and mining value chain.

Category leaders: Cyclic Materials, IonomrGrid integration. One of the hardest to crack. Canada’s multi-jurisdictional grid complexity, centralized planning and geographic distance are real hurdles. But the tailwinds are strong. Governments are putting up billions to modernize and expand the grid. Utilities and regulators need solutions to meet demand. National programs like OERD’s Smart Grid group are pushing forward strategic bets and tackling roadblocks. Startups that crack demand response, virtual power plants, and load shifting here have a replicable playbook for fragmented grids globally.

Category leaders: Corinex, ecobee (acquired), BluWave-ai

WHO’S BUILDING

We mapped the Canadian startups and scale-ups building the clean compute stack, from clean energy to next-gen chips. See the full market map below.

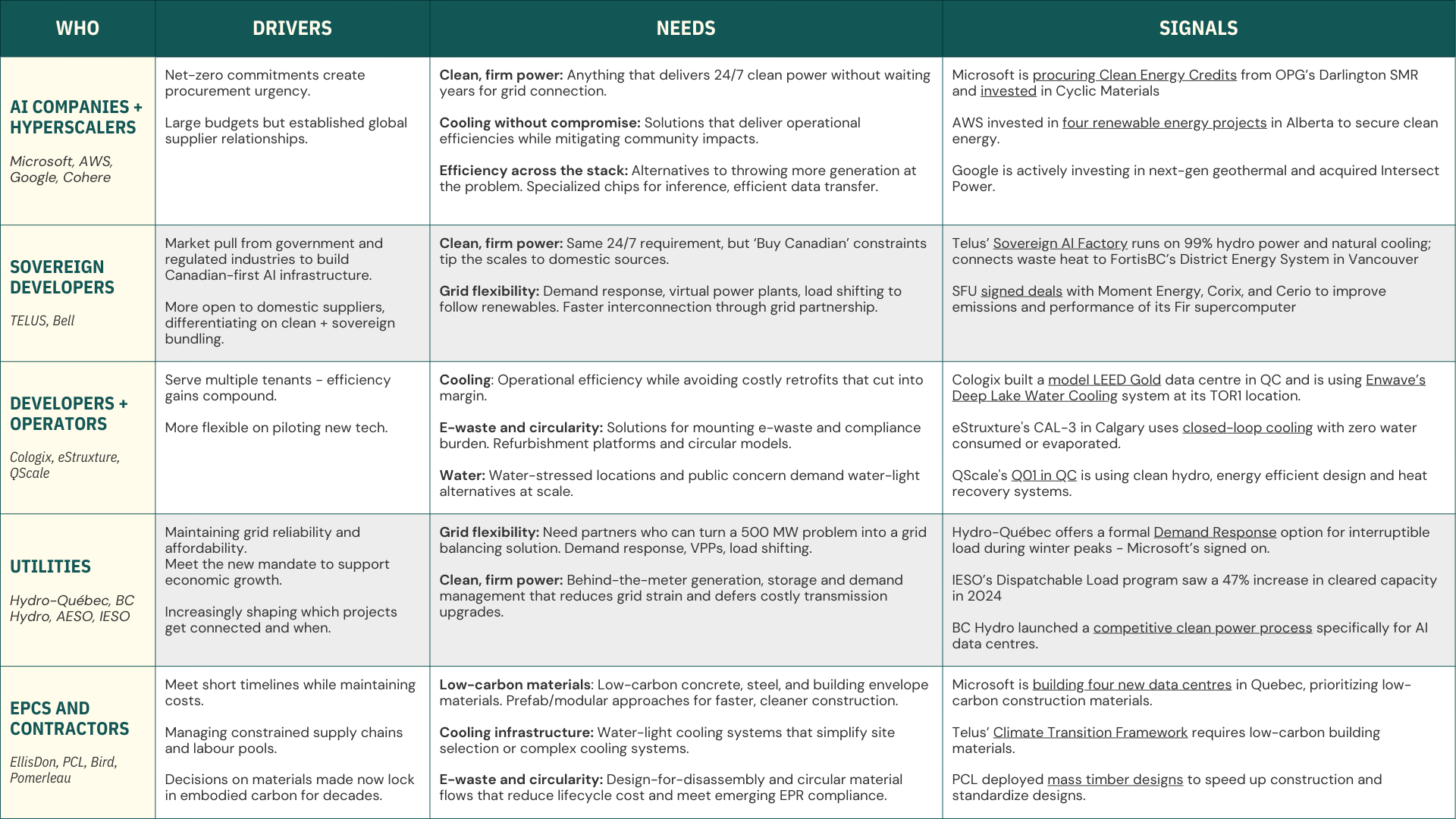

WHO’S BUYING

Each challenge and innovation opportunity has a well-funded buyer on the other side. Here’s who’s buying, what they actually need, and where Canadian startups can enter the market.

Climate Tech Canada - View Expanded

AI Companies & Hyperscalers (Microsoft, AWS, Google, Cohere)

Drivers: Net-zero commitments create procurement urgency. Large budgets but established global supplier relationships.

Needs: 24/7 clean power without waiting years for a grid connection; operational efficiencies while mitigating community impacts; specialised inference chips and efficient data transfer as alternatives to throwing more generation at the problem.

Signals: Microsoft is procuring Clean Energy Credits from OPG’s Darlington SMR and invested in Cyclic Materials; AWS invested in renewable energy projects in Alberta to secure clean energy.

Sovereign Developers (TELUS, Bell)

Drivers: Market pull from government and regulated industries to build Canadian-first AI infrastructure. More open to domestic suppliers, differentiating on clean + sovereign bundling.

Needs: 24/7 clean power where "Buy Canadian" constraints tip the scales to domestic sources; demand response, VPPs, and load shifting to follow renewables; faster interconnection through grid partnership.

Signals: TELUS's Sovereign AI Factory runs on 99% hydro power and natural cooling; connects waste heat to FortisBC’s District Energy System in Vancouver; SFU signed deals with Moment Energy, Corix, and Cerio for its Fir supercomputer

Colocation Operators (Cologix, eStruxture, QScale)

Drivers: Serve multiple tenants — efficiency gains compound. More flexible on piloting new tech.

Needs: Cooling that avoids costly retrofits cutting into margin; refurbishment platforms and circular models for mounting e-waste and compliance burden; water-light alternatives at scale for stressed locations.

Signals: Cologix built a model LEED Gold data centre in QC and is using Enwave’s Deep Lake Water Cooling system at its TOR1 location; QScale's Q01 in QC is using clean hydro, energy efficient design and heat recovery systems.

Utilities (Hydro-Québec, BC Hydro, AESO, IESO)

Drivers: Maintaining grid reliability and affordability. New mandate to support economic growth. Increasingly shaping which projects get connected and when.

Needs: Partners who can turn a 500 MW problem into a grid balancing solution via demand response, VPPs, and load shifting; behind-the-meter generation and storage that reduces grid strain and defers costly transmission upgrades.

Signals: IESO, BC Hydro, and Hydro-Québec offer formal Demand Response options for interruptible load during winter peaks - Microsoft’s committed to 30% curtailment in QC.

EPCs & Contractors (EllisDon, PCL, Bird, Pomerleau, WSP)

Drivers: Building physical infrastructure on short timelines while managing constrained supply chains and labour pools. Decisions made now lock in embodied carbon for decades.

Needs: Low-carbon concrete, steel, and envelope materials with prefab/modular approaches; water-light cooling systems that simplify site selection; design-for-disassembly and circular material flows to reduce lifecycle cost and meet emerging EPR compliance.

Signals: Telus’ Climate Transition Framework requires low-carbon building materials. PCL deployed mass timber designs to speed up construction and standardize designs.

RISKS AND UNKNOWNS

These are the real risks and unknowns for founders and investors evaluating the market:

Will your buyers actually build? Hyperscalers are announcing GWs of projects, but it’s unclear how much will actually get built. Interconnection queues hold GWs of projects, but grid connections take years and face community scepticism. If you’re building a product around data centre demand that doesn’t materialize on schedule, your revenue timeline slips with it.

Long sales cycles will test your runway. Utility and enterprise buyers move slowly. 12-24 month cycles are common. If your pilot takes 18 months and your next round takes another 24, you need 3-4 years of runway. Procurement inside hyperscalers is often disconnected from the innovation team that ran the trial.

“Sustainability” alone won’t close a deal. Speed to power is. Solutions need to accelerate deployment and solve real operational and financial challenges - while also delivering sustainability wins.

Know your buyer. Five-nines of uptime. Tight construction timelines. Incentives spread across multiple stakeholders (developer, operator, tenant, utility). Selling into this ecosystem means knowing who actually holds budget authority and building relationships with all of them.

Regulatory fragmentation adds overhead. Fast grid connections, permitting for clean energy projects, and power purchase agreements are key conditions for data centre customers choosing where to build. Utility and regulator choices will impact the speed and scale of the market opportunity. Each province is effectively a separate market with its own compliance overhead.

The valley of death is real. Liquid cooling, utility-scale storage, and waste heat recovery are technically viable but not yet standard. Startups need pilots with credible operators and a clear path to procurement - not just validation.

WHY CANADA IS READY TO LEAD ON CLEAN COMPUTE

The opportunity is large and near-term, but why Canada specifically? The same factors drawing hyperscaler investment here also give Canadian startups structural advantages that are hard to replicate elsewhere.

COMPETITIVE ADVANTAGES

Clean grid: Quebec and BC run on 90%+ non-emitting electricity, Ontario sits near 85%. Alberta’s grid is majority fossil, but its land availability and streamlined permitting are attracting the largest queue of proposed projects. Taken together, Canada still offers the lowest-carbon compute environment in the G7

Cold climate: Free cooling via outside air and cold water cuts cooling energy loads 30-50%, a structural cost advantage over US Sun Belt markets

Sovereign edge: Federal and provincial data residency requirements create a captive market for Canadian-built solutions - and homegrown AI leaders like Cohere are already proving the model

Canadian startups have a growing sovereign advantage: federal and provincial governments prefer Canadian vendors for sensitive infrastructure. Climate tech startups selling efficiency, renewable integration, or carbon management can command premium pricing by bundling "Made in Canada" with sustainability benefits.

INNOVATION ECOSYSTEM

AI research density: Canada ranks 3rd globally for top-cited AI researchers and the fastest-growing AI talent concentration in the G7. Three national AI institutes (Mila, Vector, Amii) anchor a $2.4B federal AI strategy, including $2B for sovereign compute infrastructure.

Climate tech pipeline: Canada ranks 2nd globally on the Global Cleantech Innovation Index, with 9 companies on the 2026 Global Cleantech 100.

R&D incentive stack: SR&ED refundable tax credits, 30% Clean Technology Manufacturing ITC, 15% Clean Electricity ITC, and NRC-IRAP grants create layered support from lab to commercialization.

MARKET OPPORTUNITY

Domestic demand: 9+ GW in the pipeline, 400% projected demand growth, and $100B+ in committed investment create a well-funded near-term buyer base

Buyer diversity: Hyperscalers, sovereign developers, colocation operators, utilities, and EPCs all need solutions, creating multiple entry points for startups at different stages

Export opportunity: Canada exported $20.2B in clean energy technology products in 2024. It’s not just a domestic market - Canada’s clean compute tech stack can power infrastructure globally.

GAPS TO ADDRESS

Regulatory fragmentation & speed: Interconnection rules, tariff structures, and permitting timelines differ across every jurisdiction, creating compliance overhead that slows startups down. New models require nimbleness and support for innovation from regulators and utilities.

Pilot-to-procurement gap: Risk-averse buyers mean strong pilots don't automatically convert. Startups need funded pathways from validation to scale.

Low-carbon energy vs natural gas incentives: Canada’s clean energy and carbon pricing regime offer a strong backbone for clean compute, but ample gas supply in Alberta and the flexibility it offers could lock in high-emitting infrastructure for decades.

These gaps are real, but for founders who navigate them, the competitive moat is deep.

THE BOTTOM LINE

For founders and investors, the data centre buildout is a large, near-term opportunity to capture value at scale. But the window is closing. Startups and developers are moving quickly to close these gaps, and customer needs are evolving rapidly as supply chains, grid operators, and politicians respond to pressures.

Without clean solutions that can move at the speed of deployment, the risks compound:

Sovereignty: Hyperscalers build in US jurisdictions with faster approvals and cheaper fossil power. Canadian AI companies get forced onto foreign cloud infrastructure.

Electricity backlash: Communities are already concerned about data centres driving rate increases. Political pressure could force provinces to restrict connections entirely.

Climate backslide: Corporate net-zero targets slip from 2030 to 2040. Early decisions on gas generation, diesel backup, and air cooling create 15-20 year infrastructure that blocks cleaner alternatives.

For founders who can solve specific bottlenecks at the speed operators need, the opportunity is unprecedented. Canada has the ingredients to define clean compute and build a sovereign AI advantage.

Let us know what parts resonated with you - and what you think we got wrong. Drop a note to [email protected].

Thanks to the many people who shared their insights for this piece, particularly Eric Wallace-Deering, Sam Hasty from Active Impact, and the team at Cycle Capital.

CONTINUE THE CONVERSATION

Join a curated roundtable to present key findings from the report and dig into the opportunities with founders, investors, and operators building in this space.

Spots are limited. Sign up to be notified when registration opens.